Examples of permanent capital loss.

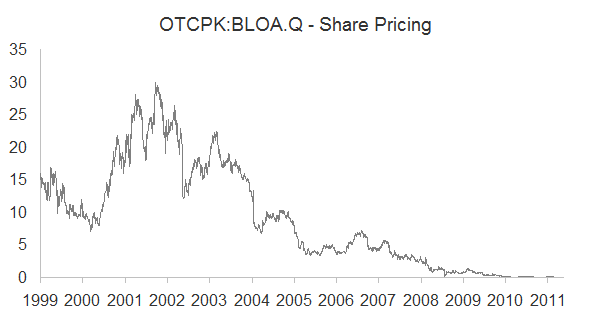

Industry Change: Blockbuster

Blockbuster was once the industry leader in home video rental. Technology has enabled cable operators to offer video-on-demand, Netflix has introduced both video streaming and a mail-order service and Redbox has introduced video rental kiosks. In short, technology advanced and Blockbuster filed for bankruptcy in September 2010. Blockbuster’s market value exceeded $5 billion in early 2002 and shareholders lost everything within a decade.

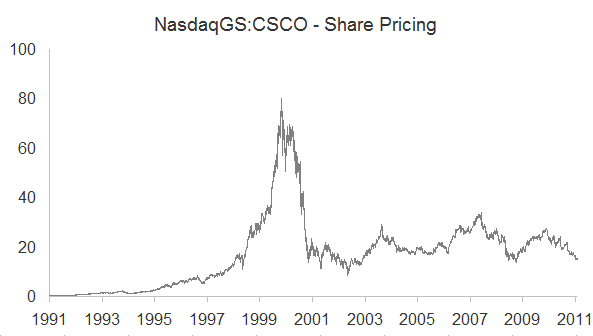

Overvaluation: Cisco Systems

Cisco Systems was a global leader in networking equipment for more than a decade prior to March 2000. Revenue had doubled and its earnings had tripled. However, in March 2000, the stock traded for almost 200 times earnings and despite a great decade of results, by mid-2011, the stock had declined 80%.

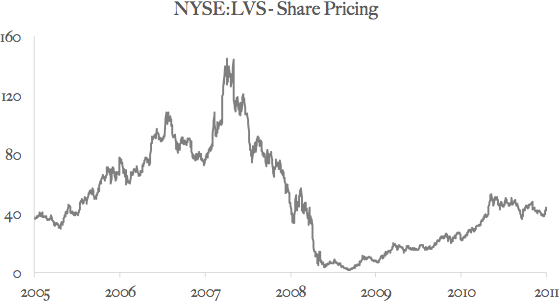

Leverage: Las Vegas Sands

Las Vegas Sands is a large casino owner/operator in both Vegas and Macau. The stock peaked at $139 in late 2007 when the company had $7.5 billion of debt against only $360 million of operating profit. When the financial crisis arrived, Las Vegas Sands’ solvency was questioned and the stock plunged below $2, a 98% decline. Despite a 20-fold increase to $40, by mid-2011 the stock remained over 70% below its peak.

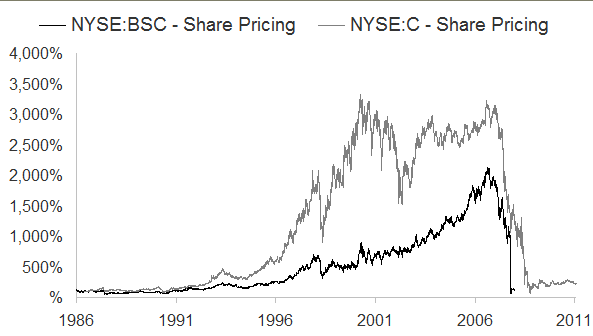

Forced Sale & Dilution: Bear Stearns and Citigroup

Bear Stearns peaked above $140 in 2007 but was forced by regulators to sell itself to J.P. Morgan for just $10 in March 2008, a 92% decline. Bear’s shareholders did not get to participate in an industry rebound because of the forced sale. Similarly, the government forced massive dilution of Citigroup’s equity in exchange for a bailout. Before stock splits, Citigroup peaked in early 2007 above $545 and by mid-2011 traded at just $38, a 93% decline.

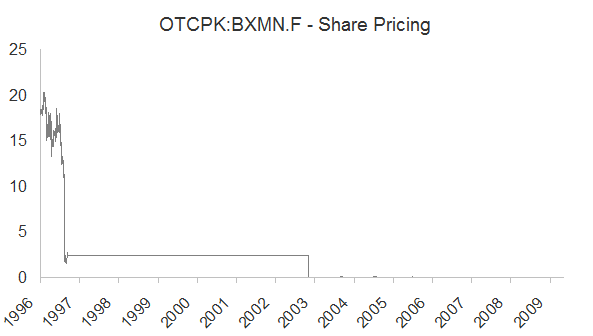

Fraud: Bre-X

The Bre-X story is well known in Canada. The company’s market value once exceeded $4 billion but quickly unraveled when the fraud was uncovered in early 1997 before the company eventually filed for bankruptcy and investors lost everything. In mineral discoveries by little known companies, it pays to be cautious. The record book is full of disappointments.

Managing Through Rising Interest Rates

Managing Through Broader Market Turbulence